Key Features

- File taxes. Allows someone else to prepare and file returns, such as income and corporate taxes with the IRS.

- Represent the taxpayer. Authorizes someone else to communicate with the IRS for tax-related matters.

- Receive notices. To request and obtain copies of IRS letters, notices, and transcripts.

- Negotiate tax issues. To handle audits, payment plans, penalties, and settle disputes with the IRS.

- Sign tax forms. Gives authority for the representative to sign tax forms on behalf of the taxpayer.

Who can represent me?

- Attorneys

- Certified Public Accountants (CPAs)

- Enrolled Agents (federally licensed tax individuals[2])

- Officers (of an organization)

- Full-Time Employees (of the taxpayer)

- Family Members

- Enrolled Actuary (under the Joint Board for the Enrollment of Actuaries)

- Unenrolled Return Preparer

- Qualifying Student or Law Graduate

- Enrolled Retirement Plan Agent

How to Write

Download: PDF

Part I – Taxpayer’s Information[3]

Section 1. Taxpayer’s Details

- Full Name

- Address

- Tax ID No. (Social Security Number or Employer Identification Number)

Section 2. Representative’s Details

- Full Name

- Address

- No. (Preparer Tax Identification Number (PTIN) or Centralized Authorization File (CAF) Number)

Section 3. Acts Authorized

- Describe the tax matters that are being handled (e.g., income), the tax form number(s), and the years represented.

Section 4. Specific Use Not Recorded

- Check this box if the designation is for a one-time or specific use case that will not be stored on the IRS CAF system.

Section 5. Additional Acts Authorized

- If the taxpayer is having their taxes filed on their behalf, check the box labeled “Sign a return.” Otherwise, enter the acts being authorized on the taxpayer’s behalf.

Section 6. Retention / Revocation of Prior Power of Attorney

- Check this box if any prior Form 2848 designation will remain in effect (by default, a newly filed version will void all previous ones.

Section 7. Taxpayer’s Signature

- The taxpayer must sign, date, and print their name.

- A wet signature is required if the representative will file this form through non-online methods (fax or mail).[4]

Part II – Declaration of Representative

- Designation

- Insert a letter, “a” through “r.”

- Licensing Jurisdiction

- Where the representative is licensed, enter the State or licensing authority.

- License Number

- BAR, license, certification, registration, or enrollment number.

- Representative’s Signature

- The representative must sign and date.

Filing with the IRS

IRS Form 2848 must be filed with the IRS to represent a taxpayer for any act between them and the IRS.

A representative has 3 ways to file.

1. File Online

- IRS Web Portal (login to submit)

2. Fax

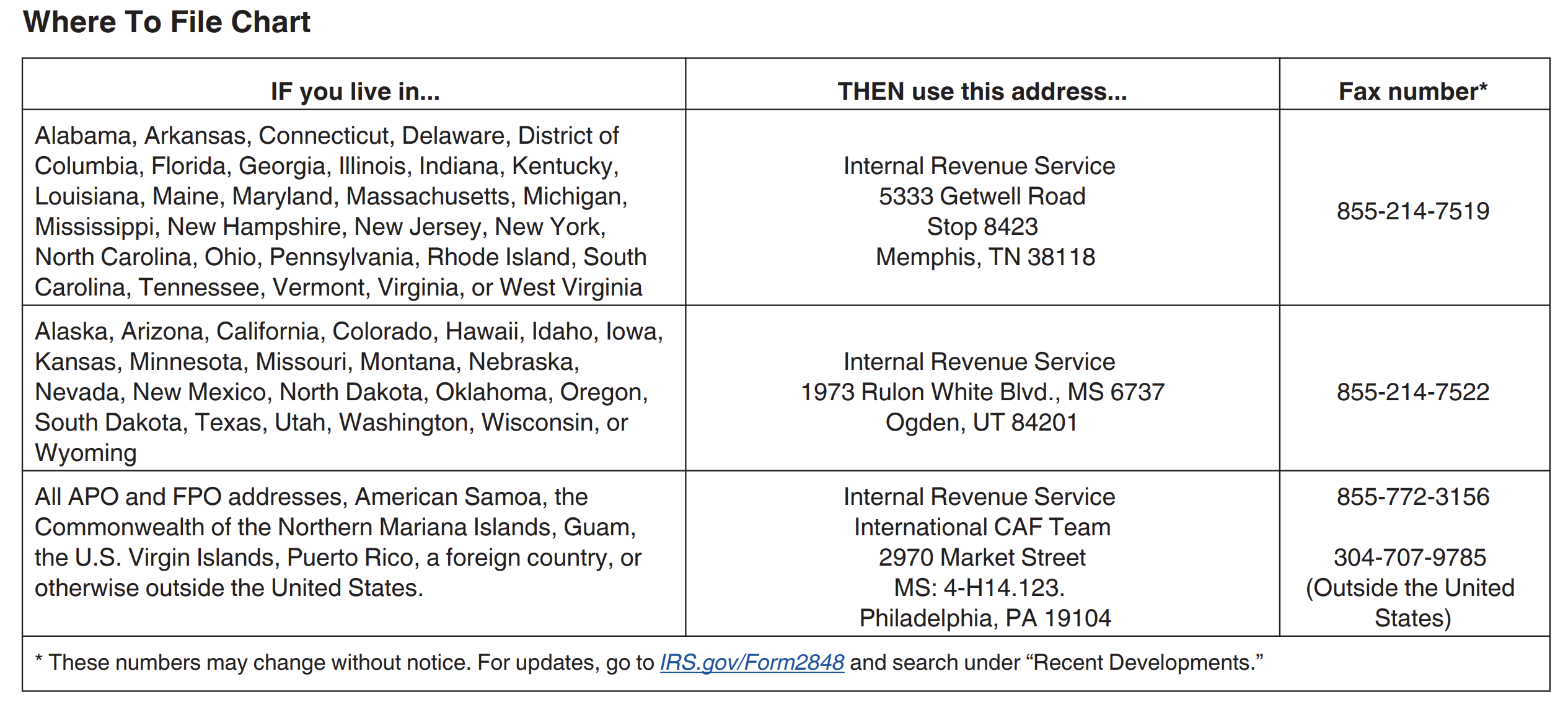

- Fax number depends on jurisdiction; see image below.

3. Mail

- Mailing address depends on jurisdiction; see image below.