IRS Form 1099-INT is a tax form used to report more than $10 in interest paid to an individual or more than $600 in interest paid to a trade or business in a year. The government agency, bank, or financial institution that paid the interest files this form with the IRS and issue a copy to the taxpayer who received the interest income.

Form 1099-INT is filed by any entity that pays interest to investors, such as a government agency or financial institution. It should be used to document amounts of at least $10 paid to an individual, such as interest paid on a savings account or dividend, or at least $600 paid in the course of a trade or business.

A 1099-INT should also be issued to an individual for whom foreign tax on interest was withheld, or federal income tax was withheld under the backup withholding rules.[1]

The recipient of a 1099-INT uses the information contained in the form to complete their annual income tax returns.

Deadlines

The deadline for sending 1099-INT forms to their recipients is January 31. Copies should be filed with the IRS by February 28 or e-filed by March 31.[2]

1099-INT vs. 1099-DIV vs. 1099-B

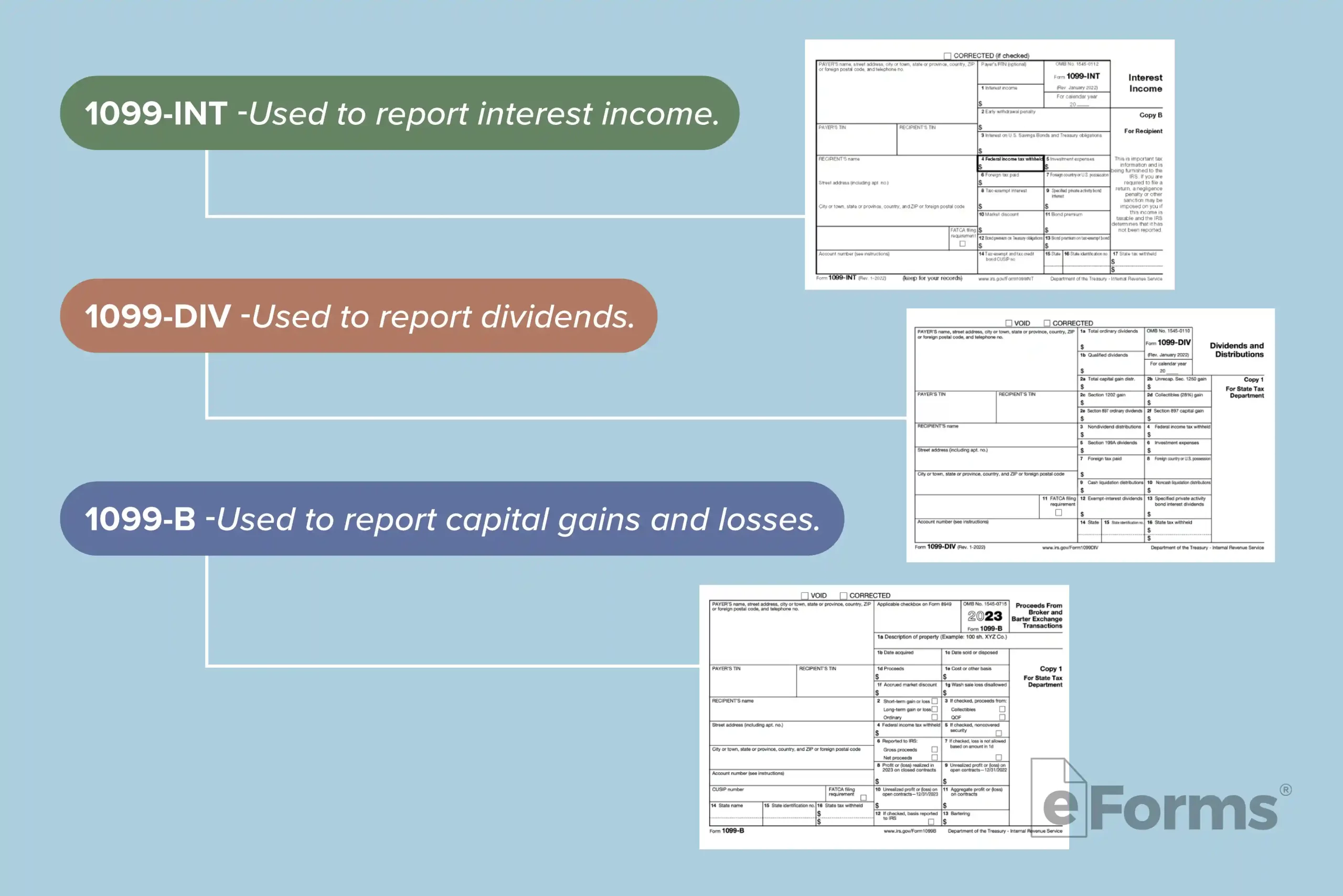

A 1099-INT is a record of income earned as a result of lending money, whether to a bank through the maintenance of a savings account or to a company through the purchase of a bond. A 1099-DIV, on the other hand, documents dividends, or the income earned through the purchase of stock. A 1099-B records capital gains and losses incurred as a result of the sale of an asset, such as stocks or bonds.

1099-INT: Used to report interest income. 1099-DIV: Used to report dividends. 1099-B: Used to report capital gains and losses.

1099-INT Form Parts (25)

1. Payer’s Information

Enter a name, address, ZIP code, and telephone number for the payer, or the institution that paid the interest.

2. Payer’s TIN

Enter the filing party’s Taxpayer Identification Number (TIN).

3. Recipient’s TIN

Enter the recipient’s TIN, which can be a social security number, individual taxpayer identification number, adoption taxpayer identification number, or employer identification number.

4. Recipient’s Information

Enter a name, address, ZIP code, and telephone number for the recipient, or the taxpayer to whom interest was paid.

5. FATCA

Check this box if the filer is a foreign financial institution reporting payments to a U.S. account.

6. Account Number

Enter an account number if multiple forms are filed for the same recipient or the FACTA checkbox is checked.

7. 2nd TIN Notice

Enter an “X” if the IRS sent two notices within three years indicating that the recipient provided an incorrect TIN.

8. Payer’s RTN

Enter a routing and transit number to participate in the program for direct deposit for refunds. Completing this box is optional and depends on preference.

9. Interest Income

Enter the amount of taxable interest paid, such as interest paid or credited by savings and loan associations, mutual savings banks, building and loan associations, cooperative banks, homestead associations, credit unions, or similar organizations.

Include interest on bank deposits, accumulated dividends paid by a life insurance company, and indebtedness (including bonds, debentures, notes, and certificates other than those of the U.S. Treasury).

Do not include interest earned on U.S. savings bonds, Treasury bills, Treasury notes, and Treasury bonds.

10. Early Withdrawal Penalty

In this box, input penalties charged for withdrawing money from a time-bound account, such as a Certificate of Deposit (CD), before its date of maturity. These will be deducted from the taxpayer’s gross interest income.

11. Box 3

Enter the dollar amount of interest earned on U.S. savings bonds, Treasury bills, Treasury notes, and Treasury bonds. Some of this is tax-exempt.

12. Federal Income Tax Withheld

Report any federal income tax withheld by the agency or institution filing the 1099-INT.

13. Investment Expenses

Input any expenses related to REMICs, or Real Estate Mortgage Investment Conduits, which are debt instruments that pool mortgage loans.

14. Foreign Tax Paid

Input, in U.S. dollars, the amount of any foreign tax paid on interest.

15. Box 7

If there was any foreign tax paid on interest, enter the name of the country or U.S. possession to which it was paid.

16. Tax-Exempt Interest

Tax-exempt interest of $10 or more should be included here. This includes interest that is credited or paid on obligations issued by a state, the District of Columbia, a U.S. possession, an Indian tribal government, or their political subdivisions, or qualified volunteer fire departments to finance eligible expenditures.

A political subdivision may include port authorities, toll road commissions, utility services authorities, community redevelopment agencies, and similar governmental entities.

17. Box 9

Enter interest of $10 or more earned on private activity bonds as defined in the U.S. Code.[3]

18. Market Discount

Market discount is the difference between the amount a bond was purchased for and its value when it reaches maturity. Enter the market discount that accrued during the tax year.

19. Bond Premium

When a bond is purchased at a premium, there’s a loss at maturity; record that loss here.

20. Box 12

Leave this box blank if a net amount of interest was entered into Box 3. If not, include the bond premium on U.S. Treasury obligations.

21. Box 13

This box asks for the amortization of the interest for a tax-exempt covered security purchased at a premium.

22. CUSIP No.

This is where to enter the CUSIP number of the tax-exempt bond for which interest was paid or tax credit was allowed. The CUSIP number is a unique nine-digit identification number assigned to most financial instruments, such as stocks and bonds.

23. State

Include the abbreviated name of the state in which income tax was withheld.

If state income tax was withheld, enter the dollar amount here.

Instructions for Filers (6 Steps)

1. Collect W-9

Use Form W-9 to collect the taxpayer’s tax identification number, which can be a social security number or employer identification number.

2. Obtain Forms

Next, obtain 1099-INT forms. Fillable copies of the 1099-INT are available from the IRS.

3. Complete Forms

Complete the forms according to the instructions outlined above, which the IRS instructions explain in more detail. Check the IRS instructions for a list of entities that are exempt from receiving a 1099-INT, which includes corporations, tax-exempt organizations, and U.S. agencies.

Submit Copy 1 to the tax department in the state where the recipient’s tax returns are being filed.

6. Send to Recipient

Send Copy 2 of the 1099-INT form package to the taxpayer whose income is being reported. The recipient of the form will use the information it contains to fill out their state and federal income tax returns.

Frequently Asked Questions (FAQs)

What do I do if I earned more than $10 in interest last year but did not receive Form 1099-INT?

Contact the issuing institution if you received more than $10 in interest but did not receive a 1099-INT. Just because the issuer failed to send a form does not excuse you from paying penalties and interest on unreported income.

I received a Form 1099-INT after I filed my return. What do I do?

File Form 1040-X to amend your tax return and thus avoid penalties related to unreported income.

Are there penalties for not issuing Form 1099-INT?

Yes. Penalties are charged for each statement an issuing institution fails to provide to a recipient. The penalty amounts change annually.