What is an ABLE account?

ABLE accounts are tax-advantaged savings accounts for individuals with disabilities and their families.

Who Gets a 1099-QA?

A 1099-QA is typically issued to the designated beneficiary of an ABLE account reporting distributions. Any contributor to the account, who received a returned contribution attributable to the calendar year, also receives a 1099-QA.

Deadlines

The deadline to file Form 1099-QA with the IRS is March 1 of the following year.[1] If the deadline falls on a weekend or federal holiday, the deadline to file is extended to the next business day. However, the filer must furnish Copy B to the designated beneficiary or contributor on or before January 31.[2]

2024 Deadlines

- January 31, 2024 (recipient)

- March 1, 2024 (IRS)

Form Parts (13)

1. Gross Distribution

Enter the total amount of payments from the relevant ABLE account during the calendar year, including amounts distributed that the designated beneficiary intends to roll over to another ABLE account. The gross distribution does not include program-to-program transfers.[3]

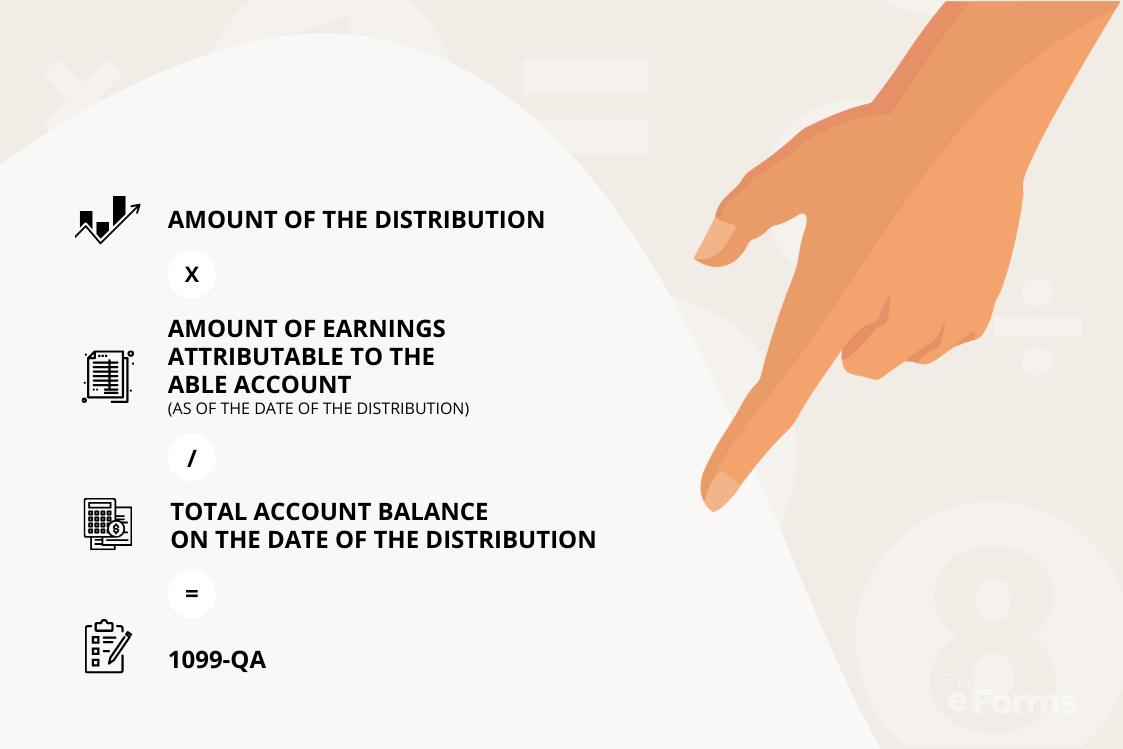

2. Earnings

The earnings portion of the distribution is calculated by multiplying the amount of the distribution (the amount in box 1) by the earnings ratio. The earnings ratio is determined by dividing the amount of earnings attributable to the ABLE account as of the date of the distribution by the total account balance on that same date.[4]

The amount to enter into box 2 can therefore be calculated using the following formula:

(Amount of the distribution) x ((Amount of earnings attributable to the ABLE account as of the date of the distribution) / (Total account balance on the date of the distribution))

3. Basis

In this box, enter the non-taxable portion of the distribution that makes up the return of investment in the relevant ABLE account. This amount is calculated by subtracting the amount in box 2 from the amount in box 1.

4. Program-to-Program Transfer Checkbox

Check this box if a program-to-program transfer was made from the relevant ABLE account to another ABLE account during the calendar year.

5. ABLE Account Terminated Checkbox

Check this box if the ABLE account was terminated during the calendar year.

6. Other Than Designated Beneficiary Checkbox

Check this box if you are filing Form 1099-QA due to a distribution to someone other than the designated beneficiary of the ABLE account (e.g., a distribution of an excess contribution to the contributor).

7. Identifying Information (6 entries)

On the left side of the 1099-QA, a total of 6 boxes require information that identifies the payer and recipient, including:

- Payer information – name, full address, and phone number

- Payer’s TIN – taxpayer identification number

- Recipient’s TIN – normally an SSN/ITIN or EIN

- Recipient’s name – full name

- Recipient’s street address – number and street only

- Recipient’s remaining address – city/town, state/province, country, Zip/postal code

The recipient’s TIN must be entered in XXX-XX-XXXX (SSN or ITIN) or XX-XXXXXXX (EIN) format on Copy A of this form.[5]

8. Account Number

The account number field is generally provided for the payer’s reference and for internal recordkeeping. It is required if there are multiple accounts for a recipient who is receiving more than one 1099.

The IRS encourages you to designate an account number for all 1099-QA forms that you file. Note that the account number must be unique and cannot appear anywhere else on Form 1099-QA.[6]

Instructions (5 Steps)

1. Collect W9

In order to have to correct information to file the 1099-QA, the payer must first collect a W9 form from the recipient. The W9 provides information needed to fill out the form, such as:

- Name

- Mailing address

- SSN/ITIN or EIN

2. Obtain the Form

Form 1099-QA is available as an online fillable PDF. If you are filing by paper, you may file a black-and-white Copy A that you print from the IRS website, along with IRS Transmittal Form 1096.[7]

3. Copy A – IRS

If filing by paper, Copy A, along with Form 1096, must be filed with the IRS by March 1. The mailing address to which you send these paper forms will depend on the home state of the filer.

4. Copy B – Recipient

Copy B must be furnished to the payee by January 31 of each year. Use the address listed on the W9 form to send Copy B to the recipient.

5. Copy C – Keep

Keep Copy C in your records for at least four years. The IRS may request the form in the event of an audit or investigation.

Frequently Asked Questions (FAQs)

Do I need to file my dependent’s 1099-QA on my taxes?

If the distributions reported on your dependent’s 1099-QA were only used for supporting a disabled individual, then the distributions are not taxable and you don’t need to report them as income.[8] Just keep the 1099-QA with your tax records.

What is the difference between Form 1099-QA and 1099-Q?

Form 1099-Q is used to report a distribution from a qualified tuition program (QTP) or a Coverdell education savings account (ESA). Form 1099-QA is only used to report a distribution from, or termination of, an ABLE account.

Can I file Form 1099-QA electronically?

Yes; as of January 1, 2023, Form 1099-QA can be filed electronically.[9]