Key Features

- Obtains the contractor’s legal name. Requests the contractor’s legal name, mailing address, tax identification number, and entity status.

- Provides accurate tax reporting. Helps to avoid inaccuracies when reporting payments made to the IRS.

- Avoids backup withholding issues. If no W-9 is collected, the payor could be subject to backup withholding up to 24% of payments made.

- Streamlines end-of-year filings. Easily file IRS Form 1099-NEC using the W-9s collected and the amount each contractor was paid.

Retention Period

A W-9 is not filed with the IRS. It is held for documentation purposes and should be kept for 4 years.[1]

How it Works (5 steps)

- Hire. Hire a non-employee (contractor) to perform services.

- Request W-9. Request a W-9 to be completed by the contractor.

- Pay. After receiving a completed and signed W-9, payment is made.

- $600 limit. If paid $600 or more per tax year, prepare 1099-NEC.

- IRS Filing. File 1099-NEC with the IRS and send a copy to the contractor before Jan 31.

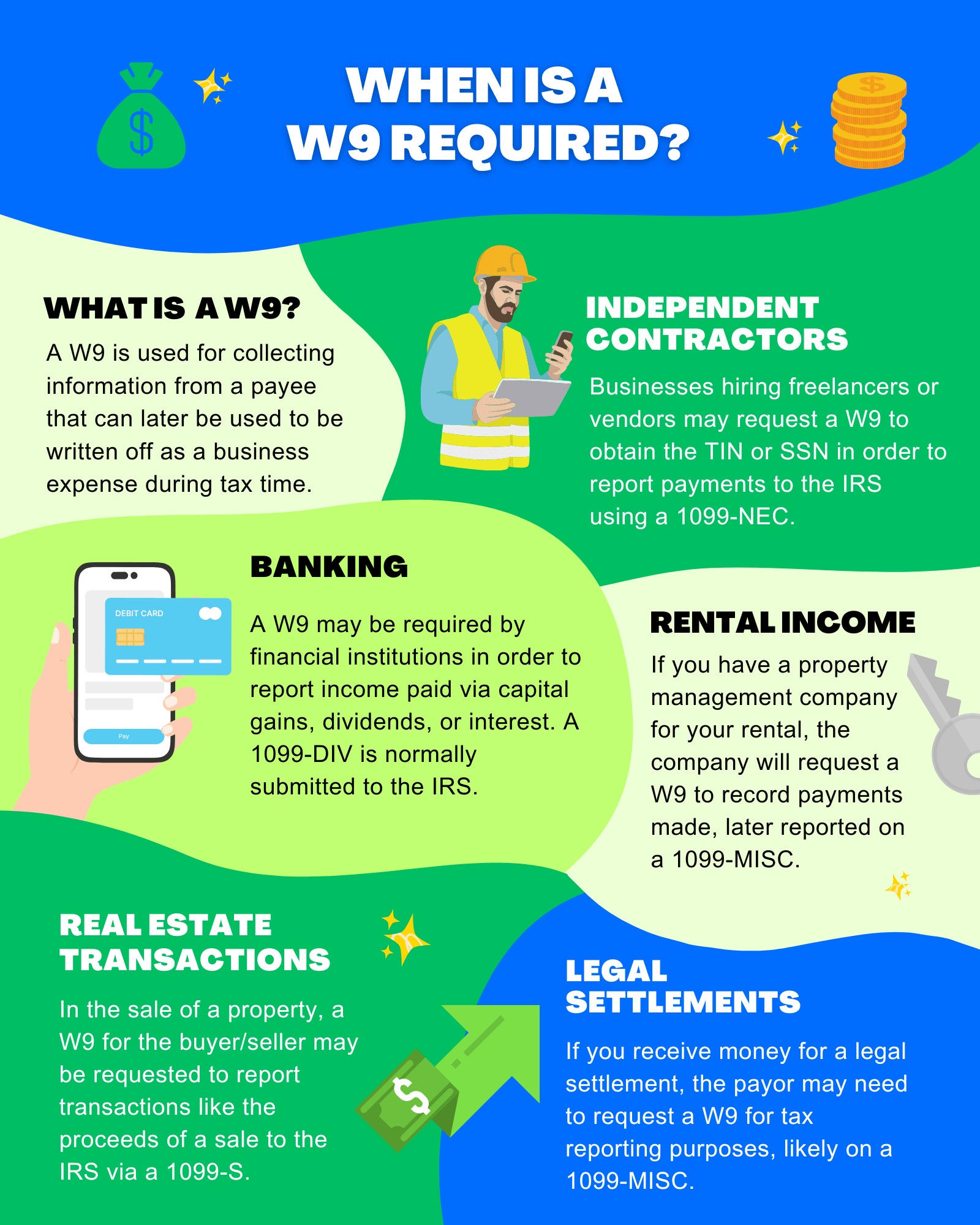

When a W-9 is Required

A W-9 must be collected if payment is being made and withholding taxes are not being deducted. Under IRS law,[2] an employer making payments for wages is responsible for collecting withholdings from employees.

After completion and signing, a W-9 requires a payment recipient to be responsible for the tax liability incurred when accepting a payment.

Common Uses

- Independent Contractors: Businesses hiring freelancers or vendors may request a W-9 to obtain the TIN or SSN to report payments to the IRS using a 1099-NEC.

- Banking: A W-9 may be required by financial institutions to report income paid via capital gains, dividends, or interest. A 1099-DIV is normally submitted to the IRS.

- Rental Income: If you have a property management company for your rental, the company will request a W-9 to record payments made, later reported on a 1099-MISC.

- Real Estate Transactions: In the sale of a property, a W-9 for the buyer/seller may be requested to report transactions like the sale proceeds to the IRS via a 1099-S.

- Legal Settlements: If you receive money for a legal settlement, the payor may need to request a W-9 for tax reporting purposes, likely on a 1099-MISC.

When a W-9 is NOT Required

- Employees: Employee-employer relationships require information about tax withholding that is completed through a Form W-4.

- Personal Payments: Payments to friends or reimbursing someone for personal services do not usually require reporting of payments.[3]

- Tax-Exempt Organizations: Payments made to charities or qualified nonprofits typically do not require a W-9.[4]

- Under IRS Threshold: The IRS reporting threshold is different in some areas. Most commonly, businesses paying for services do not need to collect a W-9 or report income under $600.[5]

Previous Version (2018-2023)

IRS W9 (2018-2023)

IRS W9 (2018-2023)

Download: PDF

How to Fill Out a W-9 (3 parts)

- Download: PDF

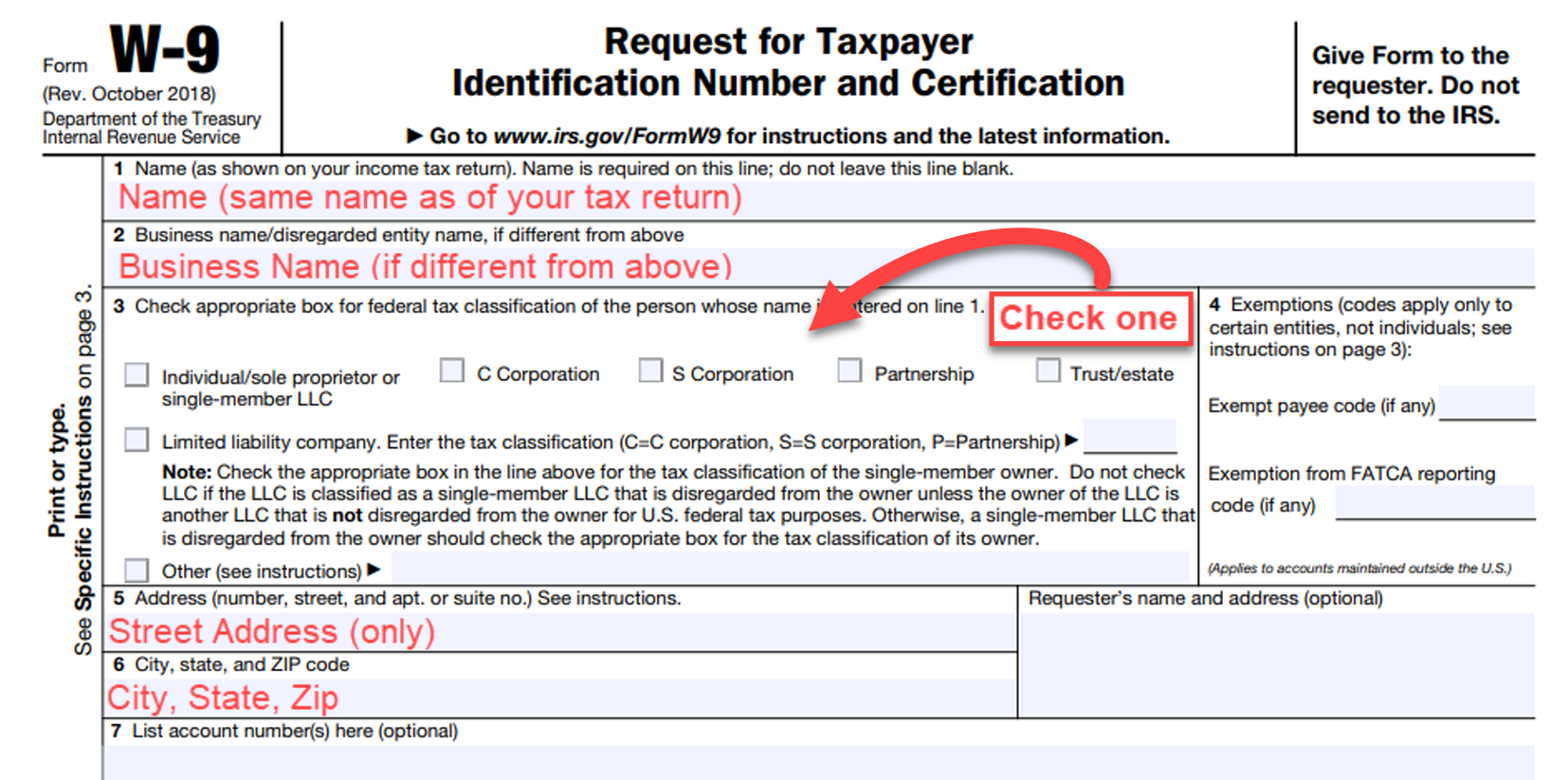

Part 1 – Identifying Information

Line 1. Name (as shown on your income tax return)

Line 2. Business name/Disregarded entity name (if different from line 1)

Line 3. Choose tax classification.

Line 2. Business name/Disregarded entity name (if different from line 1)

Line 3. Choose tax classification.

-

- Individual/sole proprietor/single-member LLC

- C Corporation

- S Corporation

- Partnership

- Trust/estate

- Limited liability company (LLC) and choose how it is taxed:

- C=C corporation

- S=S corporation

- P=Partnership

- Other

Line 5. Street Address (only)

Line 6. City, State, and Zip Code

Frequently Asked Questions

What is the penalty for not collecting a W-9?

A fine of $50 is levied on those who fail to comply with the specified information reporting requirement and collect a W-9.[6]

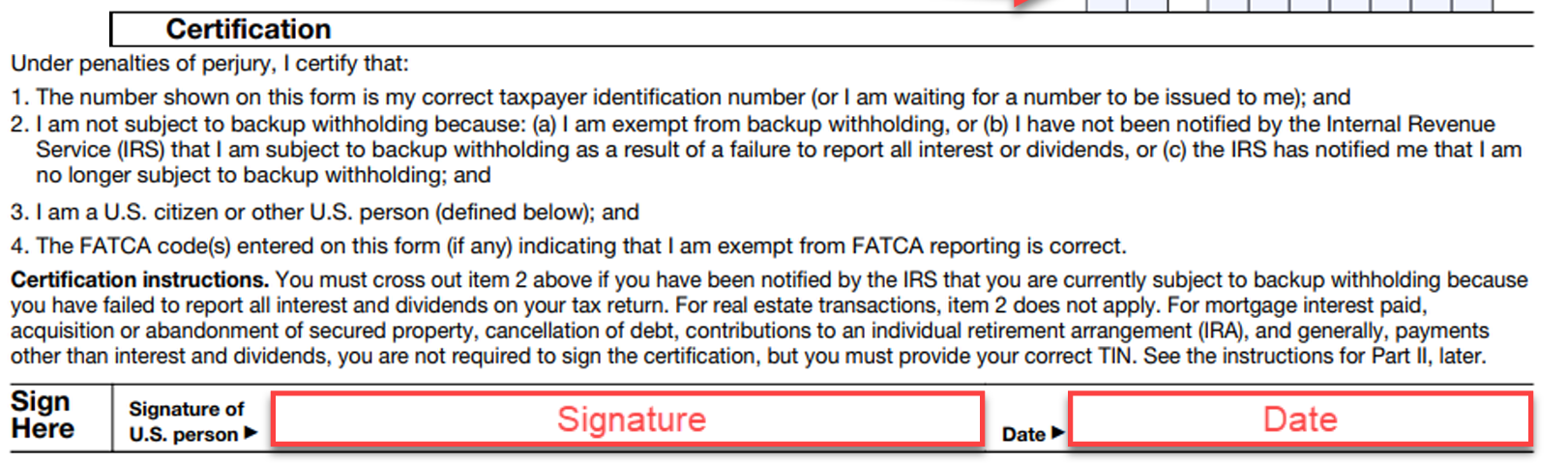

Can a W-9 be signed electronically?

The form may be signed, dated, and sent electronically and does not require a wet signature.[7]

What happens if a contractor refuses to provide a W-9?

Refusing to provide a W-9 creates compliance issues and must be handled by either:

- Backup Withholding: Invalid TINs or refusal to provide a W9 require the payor to initiate backup withholding, whereby 24% of the contractor’s payment is withheld and paid to the IRS by the payor.[8]

- Termination: The payor may terminate or suspend the vendor’s or independent contractor’s services.

What if a W-9 is incorrect?

If a W-9 provided by a payee has deliberately false information, such as a false TIN, the payee could face the penalty of perjury.[9] If a submitted W-9 has a name discrepancy or any other error, it should be resubmitted to the payor.

What happens if a W-9 is NOT collected?

If a W-9 is not collected, and transactional information is not reported to the IRS, penalties may apply.[10]

Video

Sources

- Forms and associated taxes for independent contractors | IRS

- 26 U.S. Code § 3402(a)(1)

- Paying or receiving payments from friends or family members | Taxpayer Advocate Service

- Instructions for the Requester of Form W-9 | IRS

- Reporting payments to independent contractors | IRS

- 26 U.S. Code § 6723

- Electronic Submission of Forms W-9 and W-9S | IRS

- Backup withholding | IRS

- Reasonable Cause Regulations & Requirements | IRS

- Information return penalties | IRS