By State

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- Washington, D.C.

- West Virginia

- Wisconsin

- Wyoming

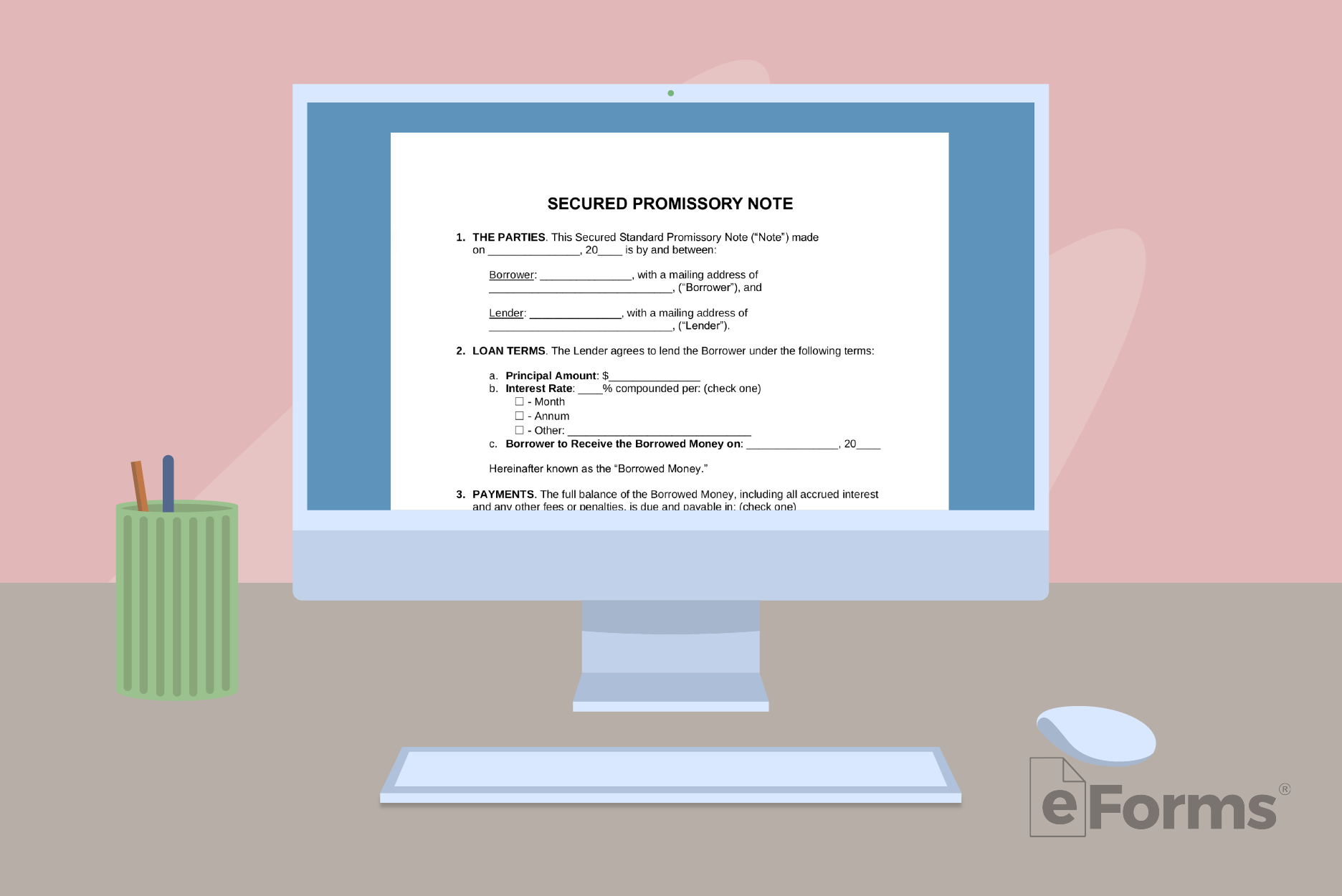

What is a Secured Promissory Note?

A secured promissory note is an acknowledgment of debt that includes collateral (security) if the borrower defaults. The note will include when the payments are due and, if paid late, the security will be handed over to the lender as a replacement for the amount owed.

How to Make a Secured Promissory Note

Step 1 – What is being “Secured”?

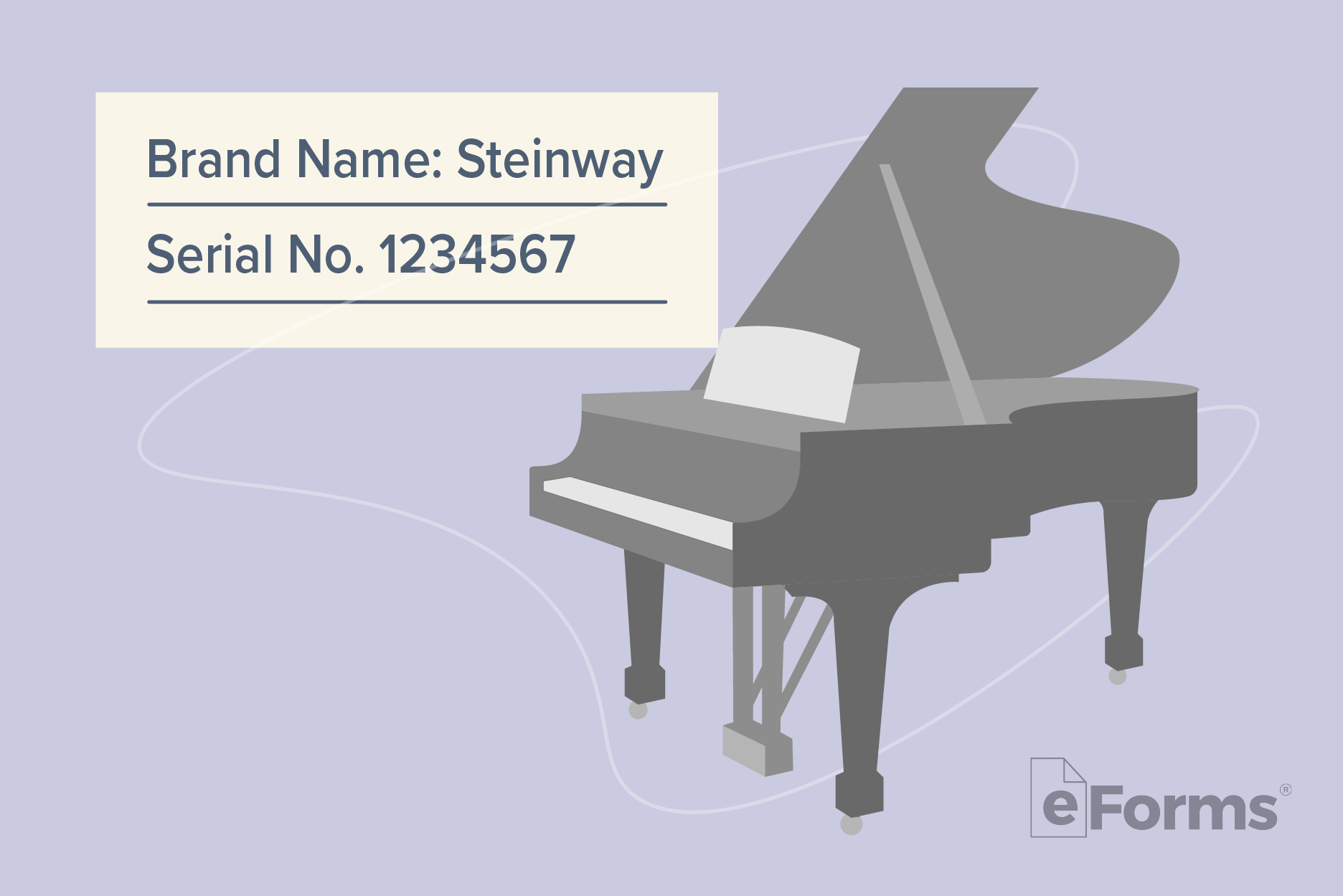

Since most promissory notes are unsecured, there should be a good reason to want them secured. The reason is; a promissory note is more casual in nature whereas a loan agreement is used more frequently when coming to terms with a secured note. A good example for the use of a secured promissory note would be for a hefty principal amount to a potentially risky borrower that owns a luxury piano. The piano, in this case, is not prone to damage, retains its value, and can be used as a security instrument. If the buyer defaults on the principal, the lender can recoup their losses by claiming the piano.

There’s no use in having a promissory note being secure if there isn’t something of equal value to the loan principal. Therefore, it’s important to have a security instrument from the borrower that backs the principal amount loaned.

Step 2 – Set Out the Terms

What makes a secured promissory note successful are the terms set out in the agreement. Below highlights all the terms set out in a promissory note. All terms should be addressed before signing the promissory note.

- Payments – Details how the principal will be paid back.

- Installments or No-Installments (No-Installments recommended)

- Interest Only payments (monthly or weekly)

- Payment upon Due Date

- Interest Due in the Event of Default – If the borrower fails to make payment when due, the lender has the option to incur an interest rate not more than defined in the State’s Usury Laws.

- Late Fees – Lender can incur a late fee if the borrower fails to make payment on time.

- Acceleration – In the event the borrower defaults on the loan, the lender can demand the total amount to be paid in full. Because this is a secure promissory note, it also gives the lender the option to claim the security instrument immediately.

Step 3 – Execute

When executing a secured promissory note, it’s important to entail as many details about the security instrument that is being attached. For example, if a valuable piano is being used as a security instrument, include as many details about the object including the brand name, serial number, and all other identifiable information.

Lenders should also consider filing a UCC Financing Statement which makes public that they have an interest in the property being used as security in the promissory note.

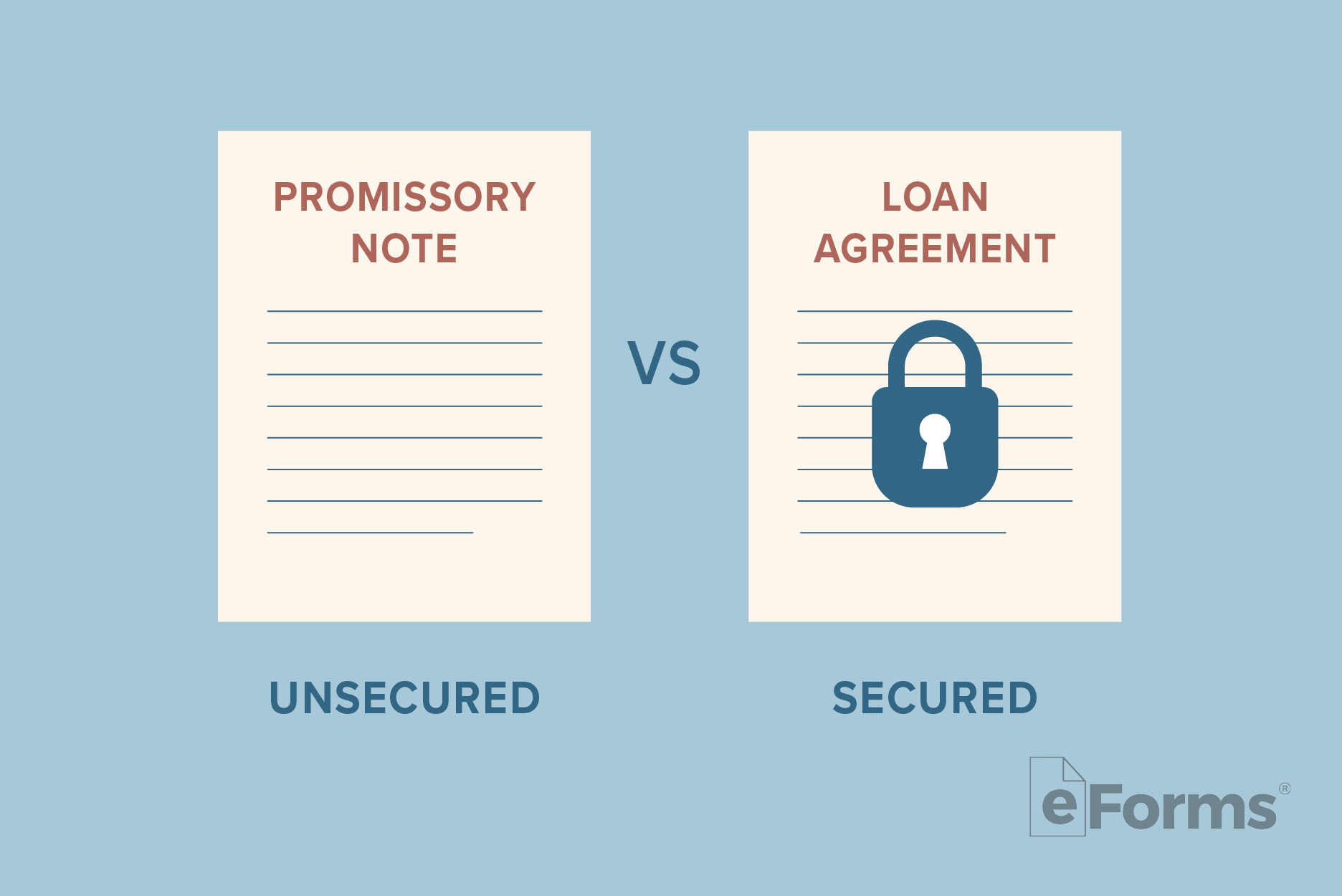

Secured vs Unsecured

Both types often include the same key elements necessary for a promissory note. However, the unsecured promissory note doesn’t offer the same assurances and securities for the lender against defaults on the loan. In other words, the unsecured promissory note doesn’t include any form of collateral.

Unsecured promissory notes have a lot more risk associated with them. Because of that, they are often used in cases where the amount of the loan is less significant, the borrower is a high-worth client with a lot of good credit, or among parties that are quite familiar with each other (i.e., friends and family).

If the loan does go into default, the lender can still file a demand for repayment, collect what’s due through a debt collection service, or settle the repayment through a small claims court. However, these processes for repayment often don’t come without their own costs. Most lenders would prefer to avoid losing more money just to make back a part of their investment (which the borrower may be completely unable to pay back).

Sample

Download: Adobe PDF, MS Word, OpenDocument