By Type (8)

Credit Report Dispute Letter – Used to dispute a claim, such as amount owed, on a credit report. Credit Report Dispute Letter – Used to dispute a claim, such as amount owed, on a credit report.

Download: PDF, MS Word, OpenDocument |

Debt Collection Letter – Used when attempting to collect a debt. Debt Collection Letter – Used when attempting to collect a debt.

Download: PDF, MS Word, OpenDocument |

Debt Forgiveness Letter – Used to exonerate an individual or party of their debt in full. Sometimes used by creditors who chooses to “write off” a debt as a loss on their taxes rather than pursue collection. Debt Forgiveness Letter – Used to exonerate an individual or party of their debt in full. Sometimes used by creditors who chooses to “write off” a debt as a loss on their taxes rather than pursue collection.

Download: PDF, MS Word, OpenDocument |

Debt Release Letter – Used as a receipt after a debt has been paid off in full. Debt Release Letter – Used as a receipt after a debt has been paid off in full.

Download: PDF, MS Word, OpenDocument |

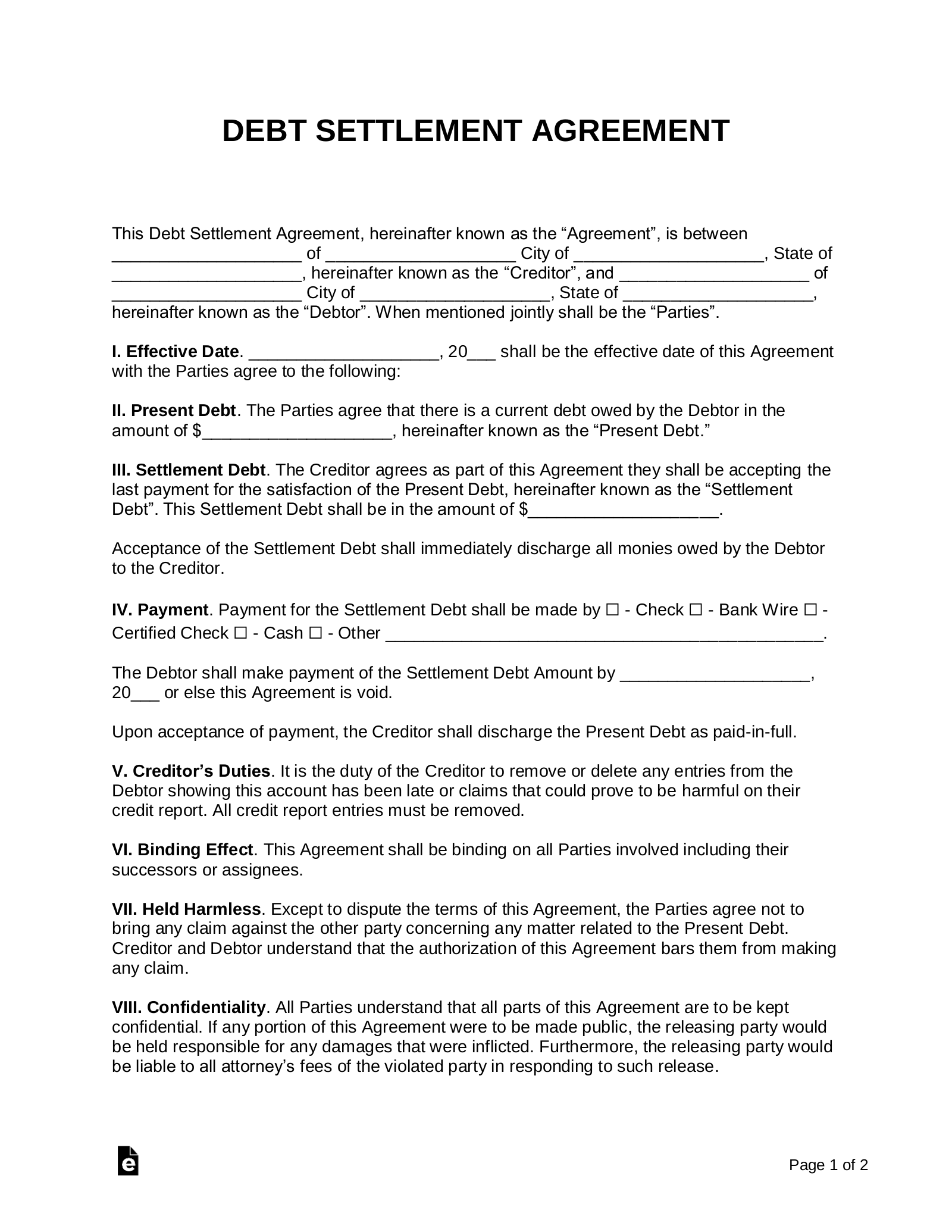

Debt Settlement Agreement – Used when two parties reach an agreement over the resolution of a debt. Debt Settlement Agreement – Used when two parties reach an agreement over the resolution of a debt.

Download: PDF, MS Word, OpenDocument |

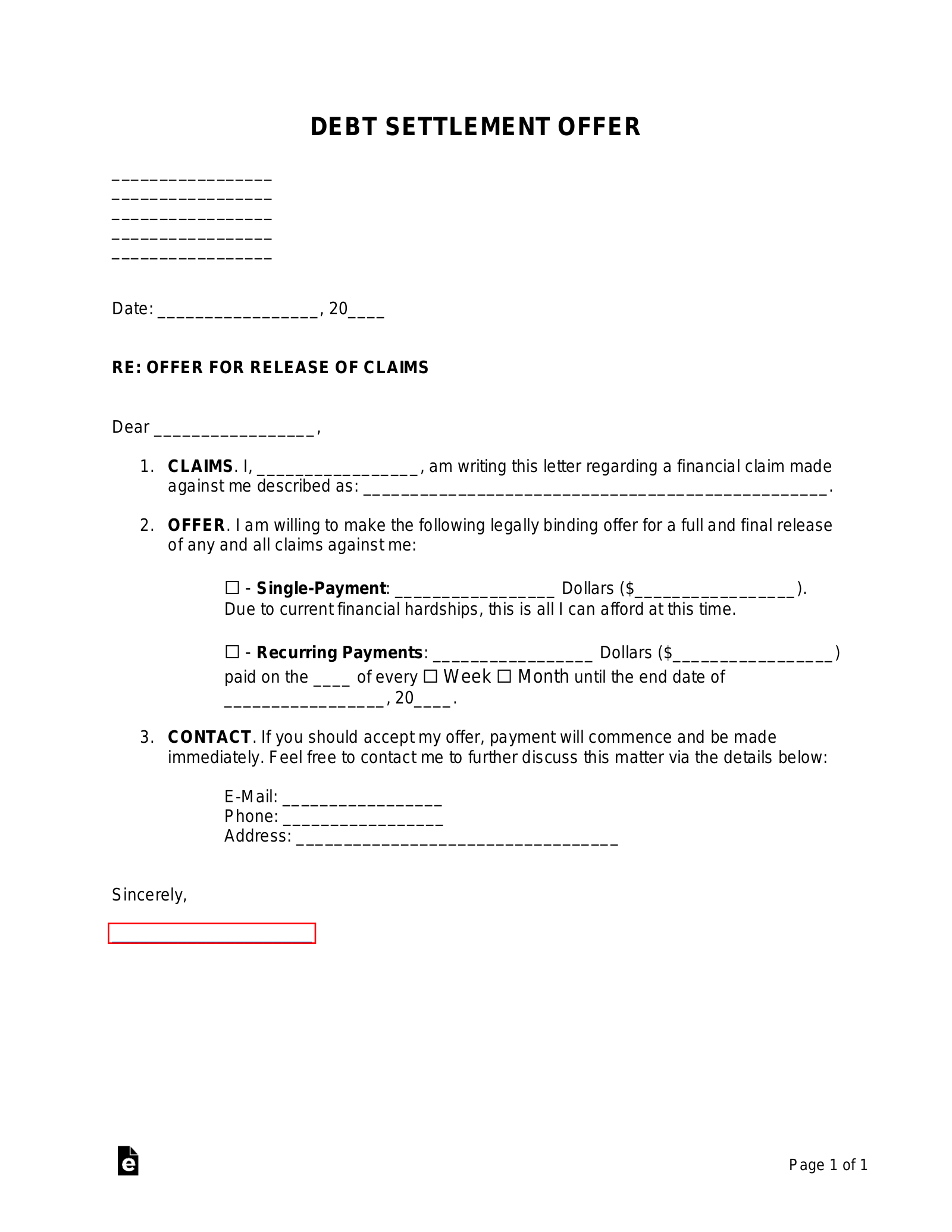

Debt Settlement Offer Letter – Used when making an offer to compromise on a debt owed. This is usually to create a new payment plan. Debt Settlement Offer Letter – Used when making an offer to compromise on a debt owed. This is usually to create a new payment plan.

Download: PDF, MS Word, OpenDocument |

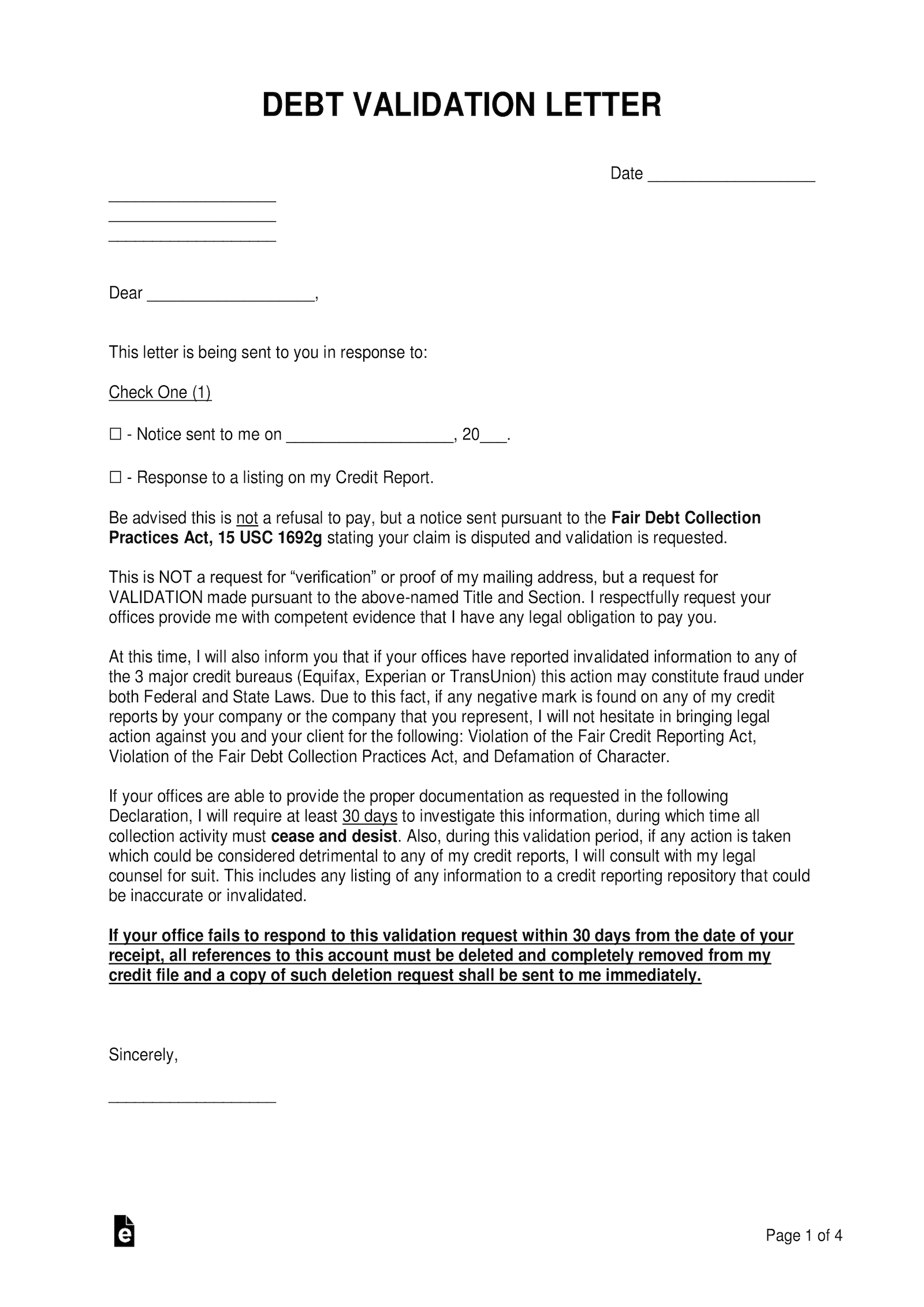

Debt Validation Letter – Used to verify a debt by requesting any and all evidence describing the debt owed. Any individual served with a collection notice reserves the right to validate their debt. Debt Validation Letter – Used to verify a debt by requesting any and all evidence describing the debt owed. Any individual served with a collection notice reserves the right to validate their debt.

Download: PDF, MS Word, OpenDocument |

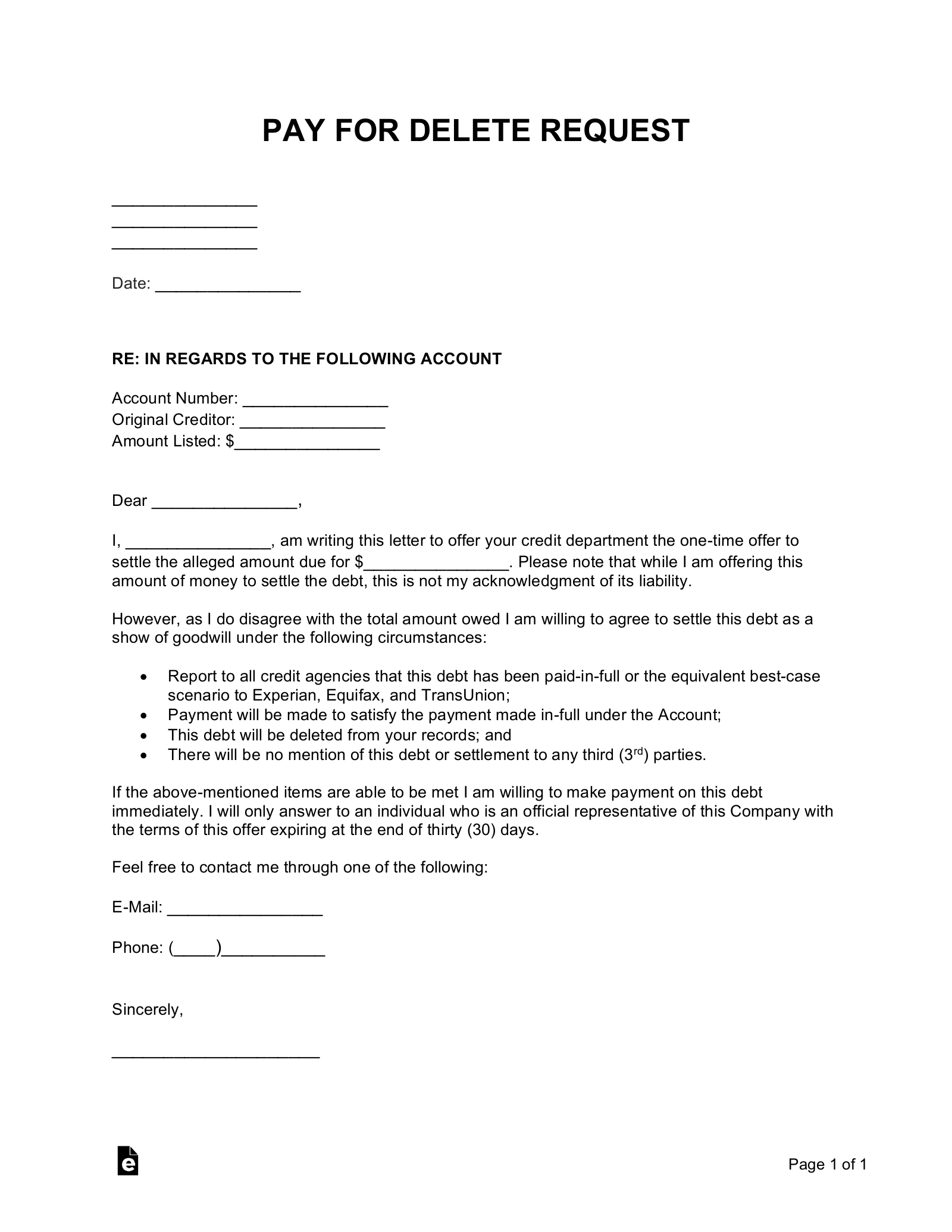

Pay for Delete Letter – Used to offer a sum to a collections agency as a settlement offer to remove the debt. Pay for Delete Letter – Used to offer a sum to a collections agency as a settlement offer to remove the debt.

Download: PDF, MS Word, OpenDocument |

How to Send a Debt Letter

Include the names and addresses of both the creditor and the debtor being addressed on the upper left corner of the letter. Entering the effective date is also helpful, especially for offers of settlement and other compromises.

Include the names and addresses of both the creditor and the debtor being addressed on the upper left corner of the letter. Entering the effective date is also helpful, especially for offers of settlement and other compromises.Step 2 – Know Your Rights

The rights of the consumer and any creditor are listed in the Fair Debt Collection Practices Act ( § 1692 to § 1692p), which requires debtors to state-specific requirements when administering a debt. Under the law, the debtor has 30 days to dispute any collection.

The rights of the consumer and any creditor are listed in the Fair Debt Collection Practices Act ( § 1692 to § 1692p), which requires debtors to state-specific requirements when administering a debt. Under the law, the debtor has 30 days to dispute any collection.

Step 3 – Offer a Settlement

Unless the creditor feels as though the debtor is credit-worthy, most debts get discounted by up to 70% if the debtor is offering a lumpsum payment. This final payment is usually difficult for any business or collections agency to give up on as so many debts go uncollected.

Unless the creditor feels as though the debtor is credit-worthy, most debts get discounted by up to 70% if the debtor is offering a lumpsum payment. This final payment is usually difficult for any business or collections agency to give up on as so many debts go uncollected.

Step 4 – Respond / Accept the Terms

If the letter is an offer, then reply with a counter-offer. If the letter is a claim, it is best to request its validation. Also, if there is any other contact on the letter, it is much better to communicate through phone or email since most companies have limited support through their inbound mailing process.

If the letter is an offer, then reply with a counter-offer. If the letter is a claim, it is best to request its validation. Also, if there is any other contact on the letter, it is much better to communicate through phone or email since most companies have limited support through their inbound mailing process.